Heikin-Ashi: Anatomy of an Edge That Dissolves Under Controls

Abstract

A previous study falsified one

symmetric Heikin-Ashi (HA) strategy family and found its drawdown reduction was an

exposure effect. This follow-up runs the discovery question — does any HA rule add

value? — as a role- and direction-resolved walk-forward factorial, and it surfaces

something that looks like a clean, mechanistic edge: the bullish colour

reversal (“green flip”) beats an EMA-cross entry on equities (44/66 OOS

stock-folds, p ≈ 0.005), the pattern tracks the direction of the flip rather

than the entry/exit role (confirmed by a short-side mirror), and it survives a

turnover-matched control and an intraday replication. A tidy result — until

the right controls are applied. Then it dissolves: (1) a raw, non-HA fast

reversal does as well or better (it beats the EMA baseline 49/66 vs the green

flip’s 44/66, and beats the green flip head-to-head) — so it isn’t Heikin-Ashi;

(2) on a point-in-time S&P universe including delisted names, the edge is

concentrated in survivors (74/107) and vanishes on delisted names (19/38, p ≈

0.56) — so it is partly survivorship; and (3) it never beats buy-and-hold.

What survives is thin and generic: a fast-reversal entry beats a slow-EMA entry on

surviving equities, modestly (≈ +0.1 Sharpe), and Heikin-Ashi is incidental to it.

The lasting value is methodological — a worked example of how a carefully-validated,

mechanistically-plausible signal evaporates under a raw-signal control and a

survivorship correction. Everything runs on the open-source

wichtelm backtester.

1. Why a second study

The first article’s verdict — “HA adds no measurable edge over an equivalent trend rule on equities” — was correct about the thing it tested: a strong-candle rule that fires HA on the way in and the way out. But “this one architecture fails” is not “HA is useless.” So this study changes the question from falsification to discovery, with the discipline the first one earned the right to demand: a pre-specified factorial, walk-forward selection, and a battery of controls — turnover-matching, a short-side mirror, transfer tests, and — decisively — a raw-signal control and a survivorship correction. The headline is not the signal it finds; it is what the controls do to it.

2. Design

The factorial. HA and the EMA-cross are made comparable by using the HA

primitive that is, like a cross, a transition event: the colour reversal

(ha_bullish_reversal / ha_bearish_reversal). The factorial swaps the signal

independently at entry and exit:

| Family | Entry trigger | Exit trigger |

|---|---|---|

d-ema (baseline) |

EMA-cross up | EMA-cross down |

d-haentry |

HA bullish reversal | EMA-cross down |

d-haexit |

EMA-cross up | HA bearish reversal |

d-rev |

HA bullish reversal | HA bearish reversal |

All long-only on the real OHLC (HA is signal-only), 100%-equity sized, same

fixed stop/take and the gap-aware protective fills from wichtelm PR #64.

Walk-forward. The core universe is 22 large-cap daily equities, 2006–2026, under

a 3-fold expanding-window walk-forward (IS 2006→2012/2016/2021; disjoint OOS

2012–16 / 2016–21 / 2021–26). Within each fold a family is swept on the in-sample

window only; the cross-instrument-robust combination (best median IS Sharpe across

the 22 names) is locked and run once on the untouched OOS window. Metrics are

recomputed from wichtelm’s per-bar equity curve (validated to match the HTML

report to 3 dp), net of a 2 bp-per-side fee. The headline test is paired per

instrument and pooled across folds into 66 observations.

The controls (§3–§4): a turnover-matched fast-EMA baseline; the short-side mirror; an intraday (1-hour) replication and a crypto transfer; a raw fast-reversal control (a non-HA short-SMA cross); and a frozen-hypothesis re-test on a point-in-time S&P universe with delisted names.

3. An apparent edge, carefully validated

Pooled across the three OOS folds, each HA family vs the matched d-ema baseline:

| HA role | OOS wins | sign-test p | median Δ Sharpe |

|---|---|---|---|

HA at entry only (d-haentry) |

44/66 | 0.005 | +0.10 |

HA at entry & exit (d-rev) |

30/66 | 0.81 | −0.03 |

HA strong, both sides (strong-lo, article 1) |

25/66 | 0.98 | −0.11 |

HA at exit only (d-haexit) |

14/66 | 1.00 | −0.21 |

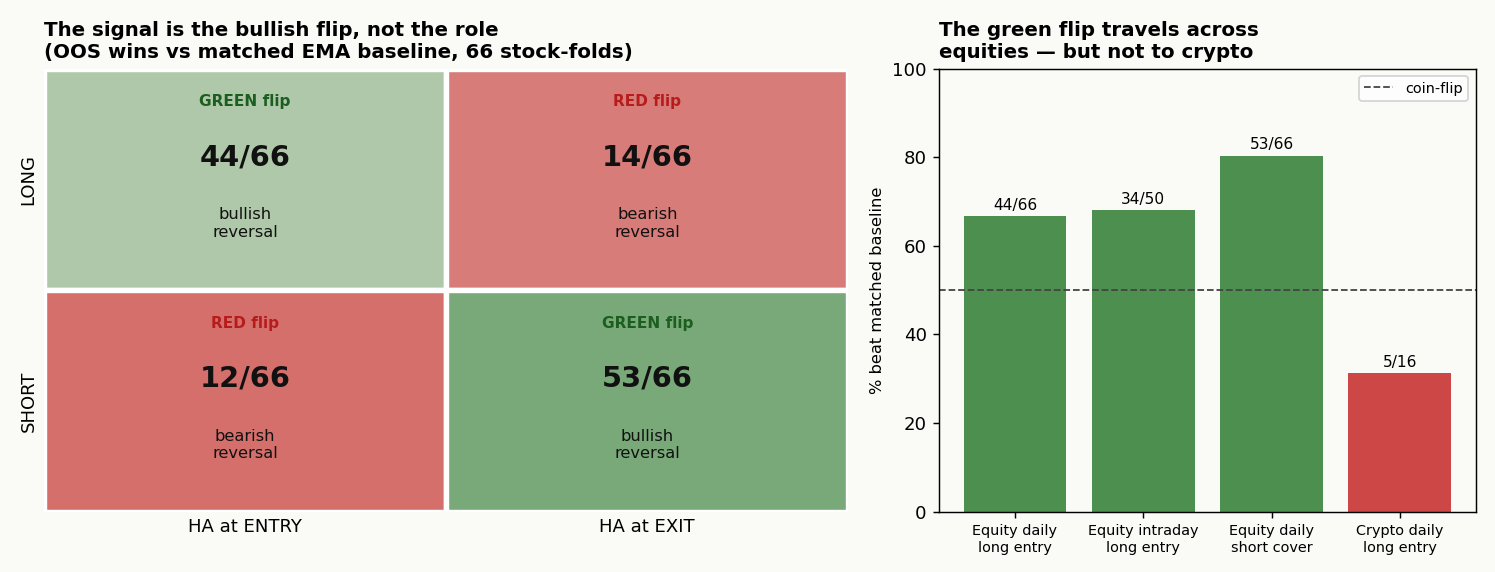

Used at the entry, the bullish reversal beats its non-HA twin; at the exit it is worse. The short-side mirror flips the pattern exactly — the value tracks the colour of the flip, not the entry/exit role: the bullish reversal wins wherever used (long entry 44/66, short cover 53/66) and the bearish reversal loses wherever used (long exit 14/66, short entry 12/66). It is not a turnover artefact — against a fast EMA matched to its trade frequency, the bullish flip still wins (long entry 46/66, short cover 58/66, p ≈ 0.001) — and it holds intraday (34/50, p ≈ 0.008), though it does not transfer to crypto (5/16).

At this point the result looks robust: pre-specified, walk-forward, turnover-matched, direction-confirmed, timeframe-replicated. The natural conclusion — the one an earlier draft of this article actually drew — is “Heikin-Ashi’s information lives in the green flip.” That conclusion is wrong, and two controls show why.

4. …and how it dissolves

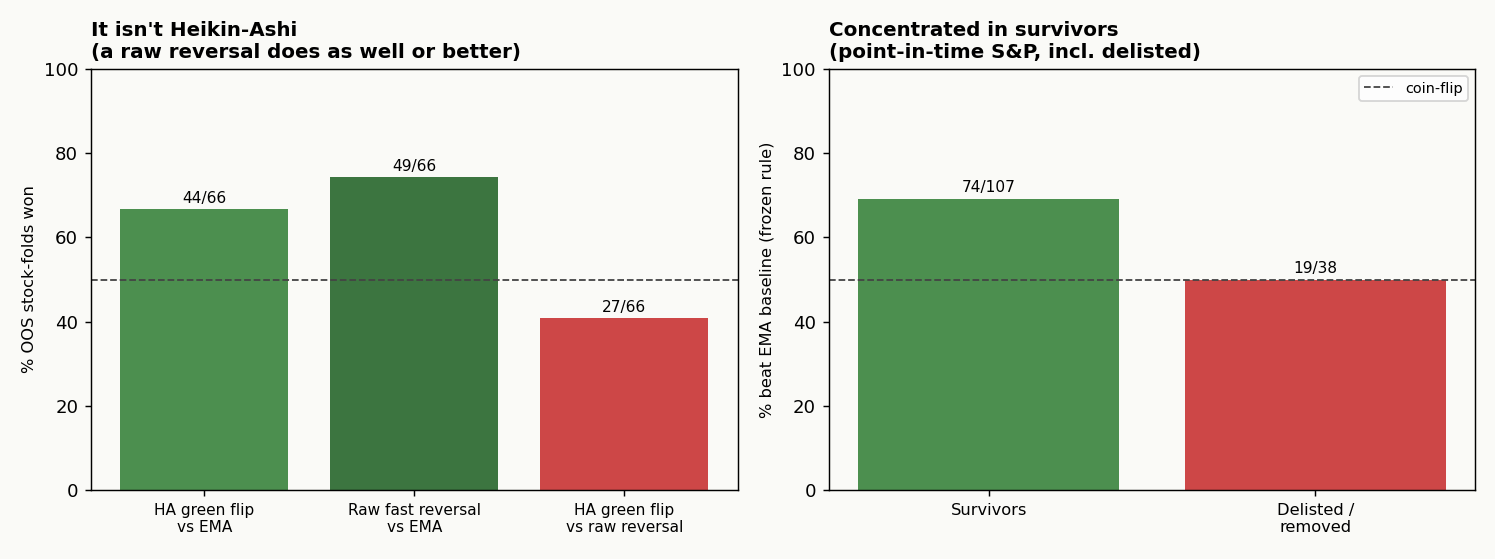

4.1 It isn’t Heikin-Ashi

Heikin-Ashi is a deterministic transform of OHLC — a recursive two-bar smoother. The

question a believer must answer is whether that specific smoothing carries

information, or whether any fast reversal detector would do. So the green-flip entry

is pitted against a raw, non-HA fast reversal: price crossing above a short SMA

(price_crosses_above_sma(2) is just “today’s close ticks up after ticking down” —

the rawest possible reversal), same EMA-cross exit and structure, same walk-forward.

| Paired comparison (OOS, 66 folds) | wins | sign-test p | median Δ net |

|---|---|---|---|

| Raw fast reversal vs EMA baseline | 49/66 | 0.000 | +18.6% |

| HA green flip vs EMA baseline | 44/66 | 0.005 | +14.5% |

| HA green flip vs raw reversal | 27/66 | 0.95 | −5.5% |

The raw reversal beats the EMA baseline more than the HA flip does (49/66 vs 44/66), and it beats the HA flip head-to-head (the green flip wins only 27 of 66). The “green flip” was never a Heikin-Ashi phenomenon — it is a generic fast-reversal entry-timing effect, and HA’s smoothing is an incidental (slightly inferior) way to compute it. The mechanistic story of §3 survives only in stripped-down form: a fast bullish reversal is an earlier entry than a slow EMA-cross, in a drifting market — nothing specific to candles.

4.2 It is concentrated in survivors

The 22-name core is currently-listed survivors, whose pullbacks, by selection, resumed — exactly the bias that would manufacture a “buy the dip’s turn” edge. To test it, the green-flip rule is frozen (a single central config, no parameter search, no peeking) and re-run on a point-in-time S&P universe including delisted and removed names, each over its full available window:

| Subset (frozen green flip vs EMA) | wins | sign-test p | median Δ net |

|---|---|---|---|

| All names (145) | 93/145 | 0.000 | +53% |

| Survivors (107) | 74/107 | 0.000 | +96% |

| Delisted / removed (38) | 19/38 | 0.56 | +0.3% |

The frozen rule does beat the EMA baseline on the broad universe — so the fast-reversal-entry effect is real and not pure parameter overfit — but it is concentrated in survivors and collapses to a coin-flip on the delisted names (19/38, median +0.3%). The “pullbacks resume” mechanism works on companies that survived; on those that died, it does not. A meaningful slice of the apparent edge is survivorship.

4.3 And it never beats buy-and-hold

Even granting the thin surviving effect, it does not make money relative to doing nothing. Three composition attempts (all walk-forward, net of cost):

- Filters make it worse. Bolting an EMA / weekly / RSI / MACD filter or a trailing stop onto the entry uniformly cuts return and Sharpe; the plain entry is best at +55% / Sharpe 0.59 and still trails equal-name buy-and-hold (+92% / 0.77), beating B&H’s Sharpe on only 19/66 stock-folds. Each filter means more time in cash → more of the drift surrendered.

- Forex doesn’t rescue it, and HA hurts there. Re-run long/short on 12 FX pairs, no variant beats a flat-ish buy-and-hold, and a plain EMA-cross (Sharpe 0.17) beats both HA variants (0.09 and −0.09). The fast-reversal edge is a drift phenomenon; strip the drift and it evaporates.

- Diversification only ties it. Pooling all 22 sleeves into an equal-weight, daily-rebalanced portfolio lifts the strategy’s Sharpe to 1.27 — but buy-and-hold’s to 1.32. The portfolio nearly matches B&H’s risk-adjusted quality at ~54% exposure and half the drawdown (−14% vs −33%), but does not beat it; the lower drawdown is the same exposure effect the first study identified (§4.2.2), since a passive B&H de-risked to 54% carries the same Sharpe.

5. What survives, and what it means

Strip away the over-attribution and the survivorship, and a single thin claim is left standing: on surviving equities, a fast bullish-reversal entry beats a slow EMA-cross entry, modestly (≈ +0.1 Sharpe), in a drifting market. It is real (frozen-hypothesis, out-of-sample), but it is not Heikin-Ashi (a raw reversal does as well or better), partly survivorship (gone on delisted names), drift-conditional (gone on crypto and FX), and not alpha (never beats buy-and-hold). The green/red asymmetry of §3 is a true description of the data, but its mechanism is reversal-timing-versus-drift, with HA incidental.

The durable contribution is methodological. The §3 result had every surface marker of rigour — pre-specified factorial, walk-forward, turnover-matched, direction-confirmed by a genuine out-of-sample prediction (the short-side mirror), timeframe-replicated — and it was still misattributed and survivorship-inflated. Two controls that retail backtests almost never run caught it: a raw-signal control (does a non-HA version do as well?) and a survivorship correction (does it hold on names that delisted?). Either alone would have deflated the headline; together they reduce a “mechanistic HA discovery” to a generic, modest, non-investable timing tilt.

6. Limitations

- The surviving claim is thin and equity/drift-specific. It is demonstrated on surviving equities in an up-drifting era; it does not generalise to crypto or FX, and it is not an alpha.

- Correlated names, nested folds. The 66 daily observations are 22 cross-correlated stocks × 3 overlapping IS folds, so sign-test p-values overstate significance; the real evidence is consistency across disjoint OOS windows, not any single p. (This cuts both ways — it tempers the apparent edge of §3 as much as the controls of §4.)

- One raw control, one universe. §4.1 uses a short-SMA reversal as the non-HA control; other smoothers (EMA-slope, smoothed typical price) are untested but would, if anything, further confirm HA is not special. §4.2’s point-in-time set still carries the first study’s data-quality caveats.

- Frozen-config sensitivity. §4.2 freezes one central parameterisation to avoid peeking; a different freeze could shift magnitudes, though the survivor/delisted split is the robust point.

- No risk-scaling, no deflated Sharpe. Fixed 100%-equity sizing; rule-vs-rule.

7. Conclusion

Asked whether any Heikin-Ashi rule adds value, this study found a signal that looked like a textbook positive result — a direction-resolved, walk-forward, turnover-matched, intraday-replicated bullish-reversal edge — and then dismantled it with its own controls. It isn’t Heikin-Ashi (a raw fast reversal does as well or better); it is partly survivorship (a coin-flip on delisted names); and it never beats buy-and-hold. What remains is a thin, generic, drift- and survivor-conditional fast-reversal entry tilt to which Heikin-Ashi contributes nothing distinctive. The honest headline is therefore not a discovery but a method: an apparent edge — even a carefully-validated, mechanistically-plausible one — should be assumed to be a mis-attribution or a survivorship artefact until a raw-signal control and a point-in-time universe say otherwise. Here, they didn’t.

Reproducibility & disclaimer

All backtests use wichtelm-app at commit

6ee5a1c (the gap-aware protective-fill build), the same build pinned by the

first study. Strategy families are

plain-text .strat files; the walk-forward harness, the raw-reversal and turnover

controls, the transfer tests and the frozen point-in-time re-test are external scripts.

Price data was snapshotted from a commercial provider and split-adjusted; the licensed

series is not redistributed, and the figures show only derived win-rates, never

prices. The point-in-time S&P membership (incl. delisted names) is the public

fja05680/sp500 dataset. Returns are net of a 2

bp-per-side fee applied post-hoc to each run’s round-trip count.

This article is for research and educational purposes only. It is not financial advice. Past performance is not indicative of future results, and hypothetical backtested results carry well-documented biases.